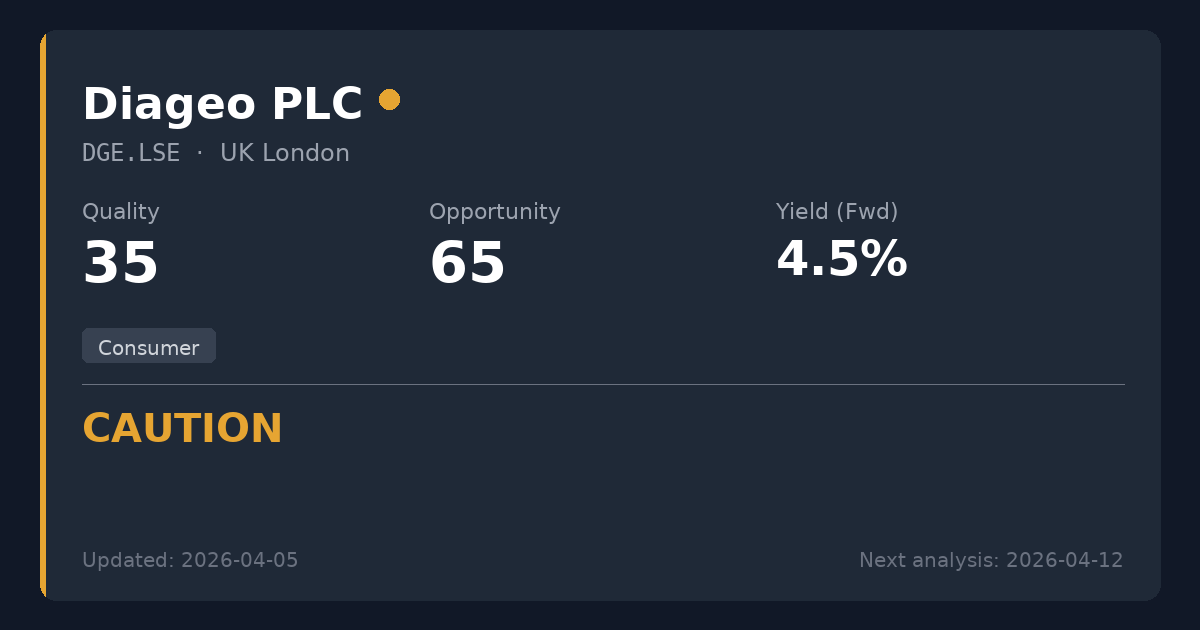

Diageo PLC

🇬🇧 DGE.LSE · London · GB0002374006

Consumer

GBX 1391.50 price at analysis

{kind=link}

Scores

Key Metrics

Powered by EODHDP/E (TTM)

13.2

P/E (Price-to-Earnings)Shows how much investors pay for each $1 of profit. We display the TTM P/E (Trailing Twelve Months) which uses actual earnings from the last 4 quarters. This is more reliable than Forward P/E which uses analyst estimates.

Calculation: 1391.50 ÷ 105.66 = 13.2

TTM period through: 2025-12-31

Forward P/E (estimated): 8.6

Based on analyst estimates

Reference: Provider P/E (Trailing): 17.2

Yield (Fwd)

4.53%

Dividend YieldThe Forward yield (Fwd) shows the next announced annual dividend / current price — what you'd earn going forward. The Trailing yield (TTM) in the tooltip shows dividends actually paid in the last 12 months. Forward is shown as primary because it reflects the company's current commitment to shareholders.

Trailing Yield (TTM): 5.95%

Net Debt/EBITDA (TTM)

3.0x

Latest quarter: 6.0x

Net Debt / EBITDAA leverage ratio showing how many years of EBITDA (earnings before interest, taxes, depreciation, and amortization) it would take to repay net debt. EBITDA approximates operating cash generation. Lower ratios (e.g., <3x) are generally safer; higher (e.g., >5x) may indicate more financial risk.

TTM through: 2025-12-31

Latest quarter (2025-12-31): 6.0x

The quarterly value can spike when quarterly EBITDA is very low (e.g., one-time charges).

Quick guide: <2x manageable, >4x can be risky (sector-dependent).

Payout (Fwd)

59.6%

Payout RatioDividends as a percentage of earnings. The Forward payout (Fwd) uses the announced dividend divided by actual past earnings (TTM) — it tells you if the company can afford what it promised. Very high payouts can be risky, especially if profits fall.

Announced dividend / actual earnings (TTM)

Payout (TTM): 97.6%

Cash Flow Payout (TTM): 53.5%

FCF Coverage (TTM): 1.17x

ROE

19.7%

ROE (Return on Equity)A profitability measure: how much profit is generated from shareholders’ equity. Higher isn’t always better if it comes from high debt.

EV/EBITDA

9.7x

EV/EBITDAA valuation ratio that compares total business value (including debt) to EBITDA. Lower can mean cheaper, but context matters.

Summary

Diageo is a global leader in premium beverage alcohol with a historically dominant brand portfolio including Guinness and Johnnie Walker. While the deeply discounted valuation (P/E 13.2) and new turnaround efforts offer a tempting recovery play, the proposed 38.9% dividend cut and severe margin contraction signal structural challenges unsuitable for strict income strategies. Not recommended for new positions in conservative dividend portfolios until the new baseline dividend proves sustainable and margins begin to recover.

Sector Context

Diageo produces, markets, and distributes premium alcoholic beverages globally, generating revenue through the sale of spirits and beers across wholesale and retail channels. In the consumer staples sector, strong brand loyalty and market dominance typically provide pricing power and stable cash flows, making them traditional dividend favorites. However, changing consumer preferences (such as the shift toward ready-to-drink beverages) and macroeconomic pressures on discretionary spending can temporarily impair margins, even for premium brands.

Temporary Opportunity Identified

Cyclical consumer demand softness in key markets and shifting consumer habits, compounded by severe margin contraction that has prompted a strategic operational and dividend reset under a new CEO.

📊 Strategy Analysis

- • Trading at a discounted TTM P/E of 13.17 and forward P/E of 8.63, reflecting significant pessimism after a multi-year share price decline.

- • The recent divestment of the IPL cricket franchise for £1.3 billion demonstrates new management's commitment to refocusing on the core beverage portfolio and reducing debt.

- • Free cash flow currently covers dividend obligations (1.17x coverage, 53.5% cash flow payout), indicating the upcoming dividend reset is a proactive strategic realignment rather than a severe liquidity failure.

⚠ What to Watch

- • The board has proposed a severe 38.9% dividend cut for 2026, breaking a reliable 10-year growth streak and making the stock unsuitable for strategies prioritizing reliable income.

- • Profitability has deteriorated sharply, with net margins compressing to 11.6% compared to a robust 5-year average of 19.8%.

- • A negative 5-year EPS CAGR (-1.4%) combined with weak US alcohol demand and shifting consumer preferences suggests fundamental headwinds requiring a multi-year turnaround.

📊 Historical Trends (10 Years)

Powered by EODHDThese charts show how key metrics have evolved over the past decade, helping you identify if the company is improving or deteriorating.

Debt Evolution (Net Debt / EBITDA)

Lower values are better. A declining trend indicates the company is reducing its debt (deleveraging).

Revenue & Earnings Growth

Consistent growth in revenueRevenue

The money a company brings in from selling its products or services. It’s the top line before costs. (blue) and earningsEarnings (Profit)

What’s left after expenses. Positive earnings mean the business made a profit; negative means a loss. (green) indicates a healthy business. Look for upward trends and recoveries after temporary dips.

Dividend Sustainability (FCF vs Dividends Paid)

Free cash flowFree Cash Flow

Cash left after the company pays for running the business and maintaining it. Often used to fund dividends, pay debt, or buy back shares. (FCFFCF (Free Cash Flow)

Short for Free Cash Flow: cash left after operating needs and maintenance spending., blue) should cover dividends paidDividends Paid

Cash the company paid out to shareholders. It’s not guaranteed and can change over time. (green). If dividends consistently exceed FCFFCF (Free Cash Flow)

Short for Free Cash Flow: cash left after operating needs and maintenance spending., the dividend may be at risk.

Analysis date: 2026-04-04

Disclaimer: This information is for educational purposes only. Not financial advice.